Developed by ISCT Business Development & Finance Committee

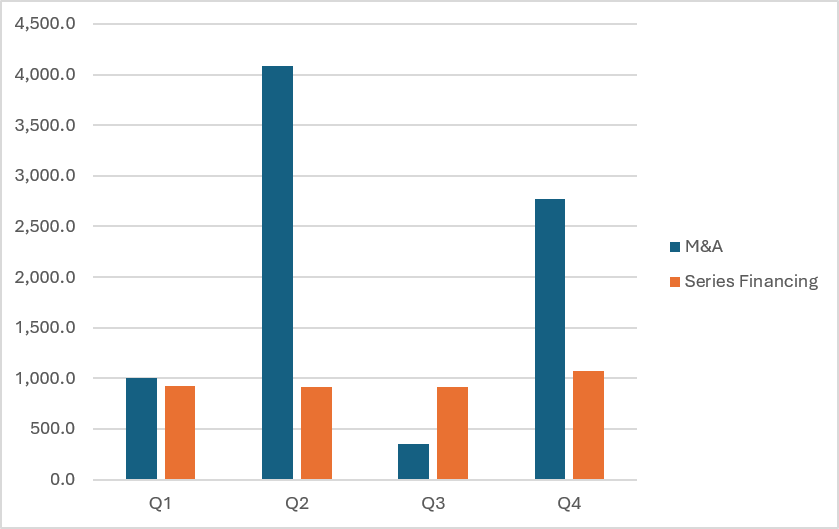

The year 2025 marked a notable period of momentum for the cell and gene therapy (CGT) sector, characterised by significant deal making across multiple therapeutic modalities. In 2025, the field saw approximately USD 12 billion in disclosed investment activity.

Series funding remained broadly stable throughout the year, at around USD 1 billion per quarter. In contrast, M&A activity peaked in Q2, driven by acquisitions of several in vivo CAR T companies. The majority of M&A deal value was concentrated in in vivo CAR T assets. Notably, EsoBiotec—an in vivo CAR T company acquired by AstraZeneca in Q1—has since released first in human data, demonstrating a favourable safety profile.

Figure 1. Capital raised via series financing and M&A deals across 2025.

Figure 1. Capital raised via series financing and M&A deals across 2025.

Overview of Deal Flow — Q4 2025

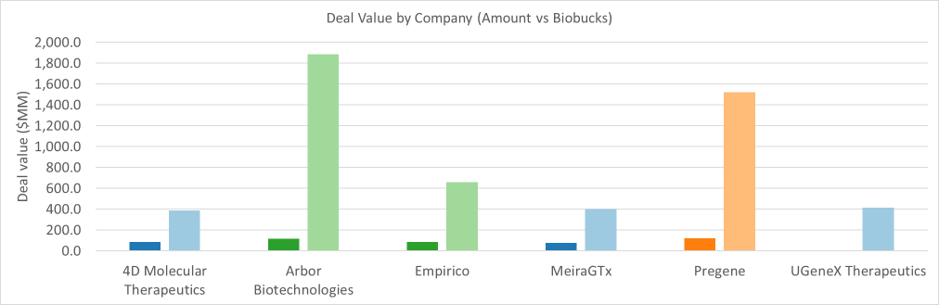

In Q4, a combined £5.1 billion was raised upfront across four major deal types (Fig 2A). Licensing contributed notable potential deal value (Fig 2B), primarily driven by milestone based structures (“biobucks”), which can be substantial but remain contingent on developmental and regulatory progress. The biggest licensing deals were for Arbor Biotechnologies ($2 billion USD) and Pregene ($1.6 billion USD) which are RNA and CAR T modalities respectively. AAV platforms were particularly popular, with half of all Q4 licensing deals (3 out of 6) involving AAV companies.

Figure 2. (A) Overview of capital raised in Q4 2025. (B) Licensing deals in Q4 2025 and associated companies. The lighter shaded columns represent “biobucks” and darker shaded represent “amount”. Blue = AAV; Green = RNA; Orange = CAR T.

Figure 2. (A) Overview of capital raised in Q4 2025. (B) Licensing deals in Q4 2025 and associated companies. The lighter shaded columns represent “biobucks” and darker shaded represent “amount”. Blue = AAV; Green = RNA; Orange = CAR T.

M&A Activity — Q4 2025

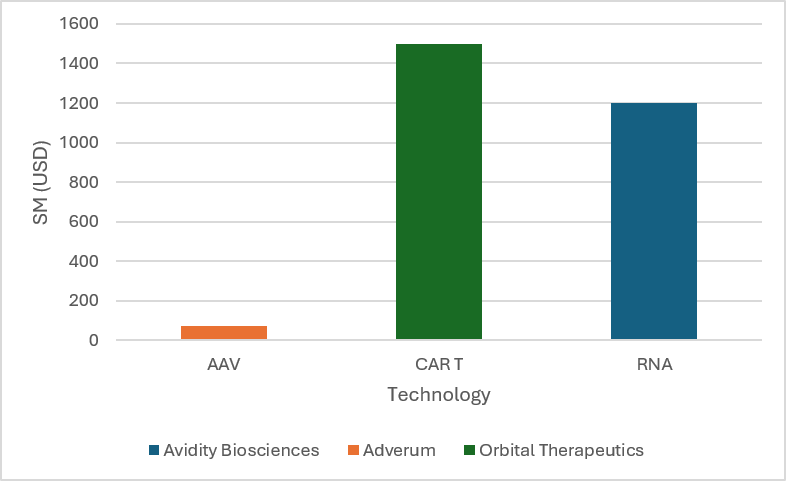

Only three M&A deals were recorded in Q4, but their scale and strategic relevance underscored broader themes shaping the CGT landscape and generated $2.8 billion.

Orbital Therapeutics led the quarter with its USD 1.5 billion acquisition by BMS, reinforcing sustained investor interest in in vivo CAR T platforms. This in vivo approach where the patient’s own body becomes the “manufacturer” of CAR T cells has the potential to expand accessibility compared with traditional ex vivo CAR T therapies.

The acquisition of Adverum Biotechnologies for USD 75 million represented the first and only AAV focused M&A of 2025. Eli Lilly offered USD 75 million upfront, with a further ~USD 200 million in milestones. This was swiftly followed by a major licensing agreement with MeiraGTx (USD 75 million upfront plus USD 400 million in potential milestones), highlighting Lilly’s evident strategic emphasis on AAV. In fact, of the six CGT investments Lilly made in 2025, half (Adverum, MeiraGTx, and Trogenix) were AAV focused.

Figure 3. M&A deals in Q4 2025 and associated companies.

Figure 3. M&A deals in Q4 2025 and associated companies.

Series Financing Trends — Q4 2025

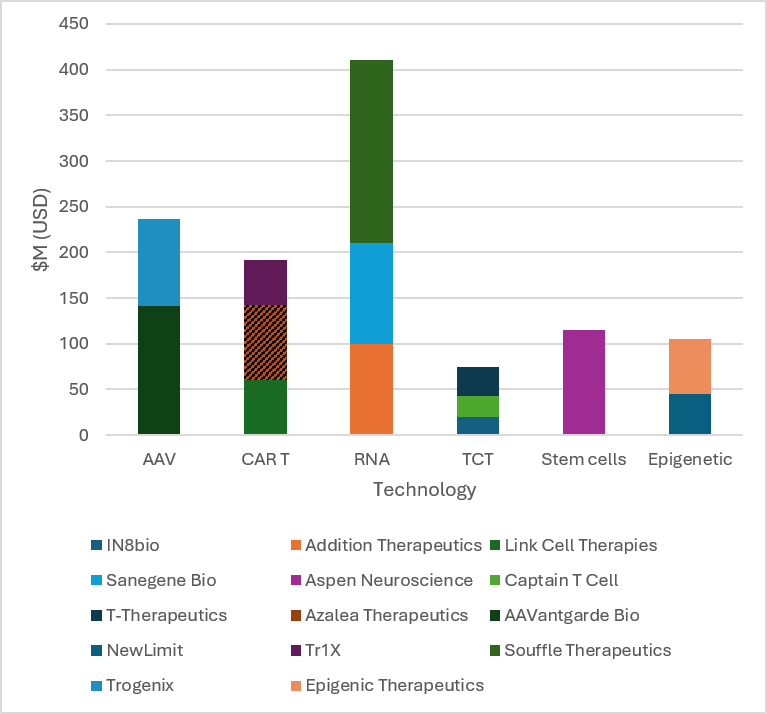

As in the previous ISCT Business Development & Finance Telegraph article, RNA, AAV, and CAR T platforms continued to dominate capital flows in 2025, raising USD 410M, 246M, and 192M respectively (Fig 4).

Figure 4. Series financing deals in Q4 2025 and associated companies.

Figure 4. Series financing deals in Q4 2025 and associated companies.

AAV: Engineering Innovation Takes Centre Stage

A clear investment trend across 2025 was a heightened focus on platform level differentiation. Targeting rare diseases alone is no longer considered sufficient; AAV companies are increasingly expected to demonstrate next generation capsid engineering or other innovative delivery strategies.

Examples include:

- Atsena Therapeutics, which raised USD 150 million in its Series C and employs a novel “laterally spreading” AAV vector.

- 4D Molecular Therapeutics, which secured two major deals during 2025 and develops synthetic capsids including aerosol deliverable AAV vectors.

- Trogenix, which leverages proprietary “synthetic super enhancer” technology for selective and potent gene regulation.

CAR T Therapy

Mirroring M&A trends, in vivo CAR T received strong attention in series financings. Investors continue to prioritise scalable, off the shelf technologies over traditional autologous platforms. In Q4, 42% of the capital raised by CAR T companies went to Azalea Therapeutics, whose dual vector system combines T cell targeted Cas9 RNP complexes with a human T cell tropic AAV vector. The use of an AAV vector is notable given that most in vivo CAR T developers (e.g., Orbital, Capstan, Stylus) rely on LNPs.

Emerging Modalities

Several more niche categories showed heightened investment momentum in Q4. While individual deals did not exceed USD 50 million, the breadth of activity was noteworthy.

Three T cell therapy modalities received financing in Q4—compared with only one such investment across the first three quarters. A potential reason is manufacturing based: T cell engager therapies, such as those from IN8bio and T Therapeutics, rely on modified antibodies, which are far easier to produce at scale than the viral vectors often required for CAR T therapies.

Two companies focused on epigenetic modulation were funded in Q4. This modality appeals to investors because epigenetic therapies offer non permanent, reversible effects—reducing long term safety risks and potentially enabling re-dosing.

Allogeneic (off-the-shelf) modalities were another strong area. Of the 12 cell based therapy financings in Q4, 9 involved allogeneic platforms. Of the remaining three, Link Cell Therapies’ logic gated CAR construct could feasibly be applied to allogeneic systems in future. The scalability advantages of allogeneic manufacturing continue to draw significant investor interest.

Conclusion

Overall, 2025 was defined by resilience and strategic evolution in the CGT investment landscape. From in vivo CAR T approaches to next generation engineered AAVs and renewed interest in epigenetics and T cell therapies, Q4’s activity highlights the expanding and increasingly innovative modalities shaping the future of cell and gene therapy.

Table 1. List of all companies and respective modalities that raised over $50 M USD in Q4 of 2025 with exceptions made for specific niche categories.

|

Company Name

|

Amount ($M USD)

|

Biobucks ($M USD)

|

Technology / modality

|

|

Transaction deals (M&A)

|

|

Orbital Therapeutics

|

1500

|

-

|

CAR T, In vivo CAR T

|

|

Avidity Biosciences

|

1200

|

-

|

RNA

|

|

Adverum

|

74

|

186

|

AAV

|

|

Equity rounds and series financing

|

|

Souffle Therapeutics

|

200

|

-

|

RNA

|

|

AAVantgarde Bio

|

141

|

-

|

AAV

|

|

Aspen Neuroscience

|

115

|

-

|

Stem cells

|

|

Sanegene Bio

|

110

|

-

|

RNA

|

|

Addition Therapeutics

|

100

|

-

|

RNA

|

|

Trogenix

|

95

|

-

|

AAV

|

|

Azalea Therapeutics

|

82

|

-

|

CAR T, In vivo CAR T

|

|

Link Cell Therapies

|

60

|

-

|

CAR T

|

|

Epigenic Therapeutics

|

60

|

-

|

Epigenetic

|

|

Tr1X

|

50

|

-

|

Allogeneic, CAR T, Treg

|

|

NewLimit

|

45

|

-

|

Epigenetic, RNA

|

|

T-Therapeutics

|

32

|

-

|

Allogeneic, TCT

|

|

Captain T Cell

|

23

|

-

|

Allogeneic, TCT

|

|

IN8bio

|

20.1

|

20.1

|

Allogeneic, TCT

|

|

Licensing and options

|

|

Pregene

|

120

|

1520

|

CAR T

|

|

Arbor Biotechnologies

|

115

|

1885

|

LNP, RNA

|

|

4D Molecular Tx

|

85

|

386

|

AAV

|

|

Empirico

|

85

|

660

|

RNA

|

|

MeiraGTx

|

75

|

400

|

AAV

|

|

UGeneX Therapeutics

|

-

|

413

|

AAV

|

|

Public offerings

|

|

uniQure

|

345

|

-

|

AAV

|

|

Capricor Therapeutics

|

150

|

-

|

Allogeneic, Exosome

|

|

Immatics

|

125

|

-

|

TCR T

|

|

Immix Biopharma

|

100

|

-

|

CAR T

|

|

4D Molecular Tx

|

100

|

-

|

AAV

|

|

Total

|

5107.1

|

5470.1

|

|

Table 2. List of identified investors and acquirers per modality in Q4 2025. Note that several modalities often overlap.

|

Modality

|

Investors

|

|

AAV

|

Eli Lilly; Schroders Capital; Atlas Venture; Forbion; Amgen Ventures; Athos KG / Athos Capital; CDP Venture Capital; Columbia IMC; Neva SGR; Sixty Degree Capital; XGen Venture; Willett Advisors; Longwood Fund; Sofinnova Partners; AviadoBio; IQ Capital; 4BIO Capital; Cancer Research Horizons; National Brain Tumour Society; Meltwind; LongeVC; Calculus Capital

|

|

CAR T

|

Johnson & Johnson Innovation; Samsara BioCapital; Sheatree Capital; Bristol Myers Squibb; Kyowa Kirin; Wing Venture Capital; Sherpa Healthcare Partners; Third Rock Ventures; RA Capital Management; Yosemite; Sozo Ventures; Select individual investors; Kite Pharma; The Column Group; NEVA SGR; Alexandria Venture Investments

|

|

EPIGENETIC

|

Lapam Capital

|

|

RNA

|

SR One; Pivotal Life Sciences; Abingworth; Osage University Partners; The Gates Foundation; BEVC; Sino Biopharm; Legend Capital; Vivo Capital; Invus; SymBiosis; Guofa Capital; TruMed; Lake Bleu Capital; Eli Lilly and Company; Qiming Venture Partners; K2 Venture Partners; TF Capital; Oriza Holdings; Northern Light Venture Capital; GSK; Novartis; Bessemer Venture Partners; Arch Venture Partners; Vida Ventures; Polaris Partners; Chiesi; Duke Management Co; Section 32; Kleiner Perkins; Dimension; Abstract; Human Capital; Boost

|

|

STEM CELLS

|

OrbiMed; ARCH Venture Partners; Frazier Life Sciences; Revelation Partners; Medical Excellence Capital; S32; Axon Ventures; LYFE Capital; LifeForce Capital; Kite (a Gilead Company); Balyasny Asset Management; Cormorant Asset Management; Prebys Ventures

|

|

TCT

|

Coastlands Capital; Stonepine Capital Management; 683 Capital Partners; Springboard Health Angels; Pluton Asset Holding AG; Sintra Limited; Technologiegründerfonds Sachsen; i&i Biotech Fund; HIL-INVENT; Brandenburg Kapital; Tencent; BGF; Sofinnova Partners; F-Prime; Digitalis Ventures; Cambridge Innovation

|

#IndustryMemberNews